Technical Support:

158-7527-1139

The winter of 2019 is quietly approaching, but the "cold winter" for air purifiers has not yet passed. In 2018, affected by the overall tightening of China's macro environment and real estate adjustments, the growth of China's home appliance market was under pressure. Relatively speaking, the healthy appliance industry performed okay, but purifiers were absent. Luftmy editor noticed that the savage growth of the air purifier market originated five or six years ago. Since the purifier market became a "pig in the path of the wind," its sales have grown alongside the increasingly severe haze weather. To combat haze, people purchased air purifiers to ensure indoor air quality.

Meanwhile, since the issuance of the "Atmospheric Pollution Prevention and Control Action Plan" in 2013, 31 provinces (regions and municipalities) across the country have continuously increased their efforts in atmospheric pollution prevention, deeply promoted urban pollution control, and effectively improved China's air quality. In 2017, the average concentration of inhalable particulate matter in cities at or above the prefecture level nationwide dropped by 22.7% compared to 2013; in 2018, Beijing had 227 days of good air quality, an increase of 51 days compared to 2013.

China's emphasis on environmental and ecological governance has gradually strengthened, with law enforcement intensity and covered areas continuously increasing. Under this influence, the purifier market experienced a cliff-like drop. According to summary data from AVC, the air purifier market shrank significantly in 2018, with a severe year-on-year decline. In 2018, total retail sales of air purifiers reached 11.67 billion yuan, a year-on-year decrease of 28.0%, with online retail sales accounting for 43.0%. The retail volume of air purifiers in 2018 was 5.291 million units, down 27.0% year-on-year, with online sales volume accounting for 61.2%. Although the market saw a slight recovery in the fourth quarter of 2018 due to recurring weather and haze, the overall downward trend of the market remains difficult to change.

According to summary data from relevant agencies, the offline scale of the purifier market in the first quarter of 2019 was 1.19 billion yuan, a year-on-year decline of 29.8%. Judging from the market growth rate, there are no obvious signs of recovery in the offline market, and purifiers are still in a low-level adjustment period. However, judging from current main-selling models in the industry, the proportion of high-end purifiers is gradually increasing, and the sales share of high-efficiency formaldehyde-removal products has risen. The online market scale for purifiers was 1.15 billion yuan, with a year-on-year growth rate of -8.2%. The decline in the online industry has further slowed down, and in March, influenced by industry promotions, a slight year-on-year increase was achieved. From the sales structure perspective, the room for downward adjustment of the average online selling price for purifiers is relatively small, and some high-end formaldehyde-removal products are gradually appearing on the charts.

According to statistics, the growth in retail volume and sales value of air purifiers in 2013 was as high as 130.6% and 162.7% respectively. In 2014, the market scale expanded and purchasing power gradually stabilized, with retail volume and sales value maintaining growth rates of 35.7% and 31.7%.

Professionals analyze that the main reason is the further deepening of the national ecological environment strategy. The guiding ideology focuses on areas such as Beijing-Tianjin-Hebei and surrounding regions, the Yangtze River Delta, and the Fen-Wei Plain, continuing atmospheric pollution prevention actions to resolutely win the battle to protect blue skies and achieve a win-win situation for environmental, economic, and social benefits.

In fact, the trend in the air purifier market showed signs of decline as early as 2015. Taking Beijing as an example, according to offline monitoring data from CMM, from 2015 to 2018, both the retail volume and retail value of the air purifier market in the Beijing area showed a downward trend. In 2015, Beijing's share of air purifier retail volume reached 21.9% and retail value 24.7%; in 2016, these dropped to 17.2% and 20.4% respectively, and the decline continued in 2017.

As early as during the "haze bonus" period, companies seeing the momentum of the "haze economy" flocked to the air purifier market, resulting in a mixed bag in the air purifier industry, with the market flooded with many counterfeit and inferior products.

Today, chaos in the air purifier market still exists. In results from multiple spot checks by relevant quality inspection departments, substandard products include not only unknown brands but also many well-known domestic and international names.

For example, a certain foreign brand has frequently failed quality spot checks by relevant departments. Investigations revealed that its production entities for air purifier products are quite complex. Luftmy editor noticed comments from home appliance industry insiders stating that the OEM production model with multiple entities, while helping companies reduce costs and move flexibly, also acts as a "Sword of Damocles" over their heads, with hidden dangers such as difficult quality control and high management complexity.

Well-known brands are becoming untrustworthy, and consumers' confidence index in the air purifier market is declining. On the other hand, improving air quality is the main reason for the decline in the air purification market.

In the past two years, the number of air purifier manufacturers has been gradually decreasing. Public data shows that in 2016, there were as many as 699 online air purifier brands and 117 offline brands. As of October 2018, the number of online brands decreased to 427 and offline brands to 103, a total decrease of 286, meaning at least 35% of brands exited the air purifier market competition. According to statistics from relevant agencies, 263 brands exited and 114 entered in 2018. Specifically, 261 online brands exited and 110 entered; 46 offline companies exited and 23 entered. These mainly fall into three categories: companies clearing inventory, those barely maintaining operations, and those seeking transformation. Brands with weak strength have been washed out in large numbers.

Regarding average prices, the average price in the online market has dropped significantly, while offline prices have fluctuated little. Analysis suggests that signs of recovery in the offline market are not obvious, and the room for price reductions for online products is already very limited.

The air purifier market urgently needs to break out of its current predicament. Some experts assert that air purifiers will certainly become a standard in every home in the future. The current difficulties in the air purifier market are only temporary, and this market still has huge untapped potential.

When air purifier products are linked with haze, consumer purchases are mostly "panic buying," which traps companies in a predicament of relying on the weather. However, expanding into market segments and creating diversified functions is expected to allow air purification companies to move away from this weather-dependent path.

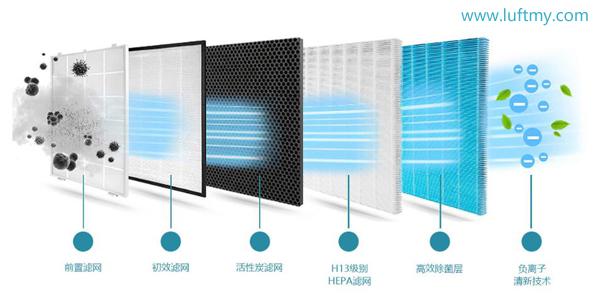

Observations show that there is still significant room for improvement between current purifiers and consumer needs. Luftmy editor noticed from consumer survey data that consumers have a strong demand for environmental monitoring. PM2.5 removal, sterilization, and formaldehyde removal remain the functions consumers care about. Currently, PM2.5 sensors have become standard in purifiers, but the ability to remove formaldehyde and bacteria still needs improvement.

On the other hand, spot check intensity must continue to be strengthened to expose problems. Clearly, industry chaos continues and cannot be cleared up in a year or two; it will take a considerable amount of time to purify the industry. Industry professionals point out that the air purifier industry is still in an adjustment period in 2019, and the industry reshuffle will continue. It is expected that the decline in the purifier market will continue to narrow in 2019, and market structural adjustment will persist throughout the year.

By pursuing high-quality focused products, positioning a good brand image, and making air purifier products refined and excellent, the development of China's air purifier market will break free from a single saturated mode and gradually transform into a mature and diversified industry, achieving an industry "warm-up."